- Personal income is the total amount of money received by individuals or households. It includes compensations from social security, welfare groups, benefits for elderly people, salaries and wages, bonuses from employment, and dividends from investments. On the other hand, disposable personal income is the amount available to be spent or saved after all mandatory deductions, such as taxes, have been made.

More often than not, individuals and households earn income, but what they earn is not always well defined. Many people are unaware of what they have earned and how they can use it. Understanding the distinction between personal income and disposable personal income is crucial for managing finances effectively.

Personal income is the total amount of money received by individuals or households. It includes compensations from social security, welfare groups, benefits for elderly people, salaries and wages, bonuses from employment, and dividends from investments. On the other hand, disposable personal income is the amount available to be spent or saved after all mandatory deductions, such as taxes, have been made.

Disposable personal income is a vital component of the economy. Individuals spend their disposable income on essentials such as food, rent, and other direct expenses. Whether spent prudently or recklessly, this money circulates within the economy, supporting various sectors. For instance, spending on alcohol supports the liquor industry, while spending on education or household items benefits other sectors.

The Circular-Flow-of-Income model explains how money moves within an economy. Individuals earn money, spend it on goods and services produced by firms, and the cycle continues.

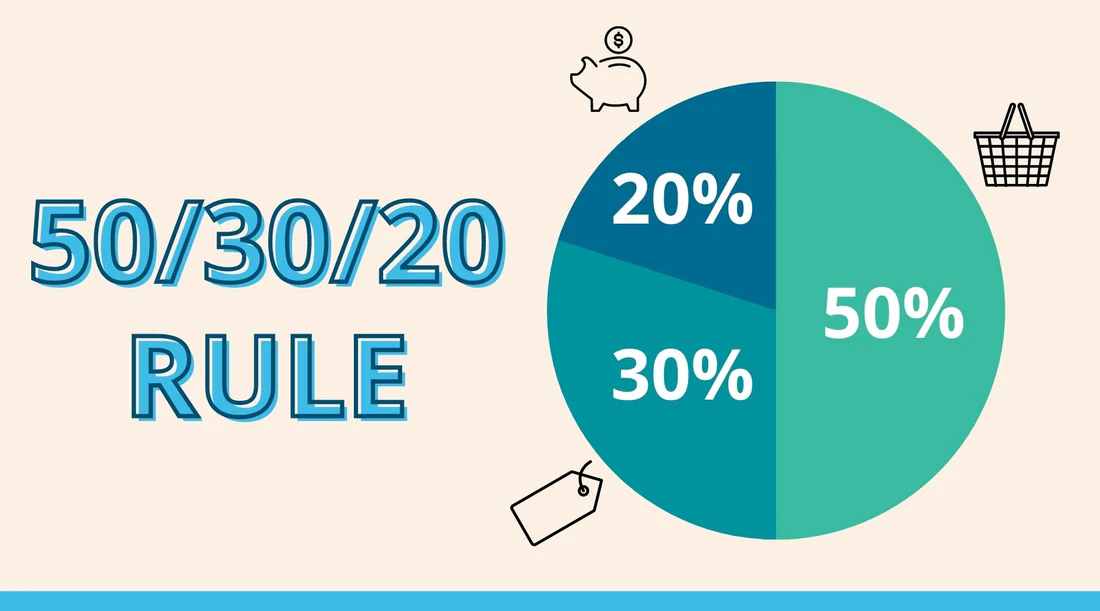

Managing disposable personal income effectively requires proper budgeting. By planning financial resources each month, individuals and households can control their finances and track their expenditure to achieve their goals. An effective budget can be built by following the 50:30:20 rule. This rule helps avoid overspending and ensures that money is allocated wisely.

Fifty percent of the budget should be spent on needs—essential items such as rent, insurance, healthcare, basic foodstuffs, minimal debt repayments, and utilities. These are necessary for maintaining a livelihood. If spending on needs exceeds 50%, adjustments should be made.

Wants, which make life enjoyable, should account for 30% of the budget. These include activities and items such as gym memberships, cars, vacations, electronics, entertainment subscriptions, and fashionable attire. While these enhance quality of life, they are not essential and can be minimized if necessary.

The remaining 20% should be dedicated to savings, investments, and emergency funds. Saving enough to cover approximately three months of expenses can provide a buffer against unforeseen events like job loss or unexpected expenditures. This also includes planning for retirement.

Adhering strictly to the 50:30:20 rule can lead to financial prudence, freedom, and prosperity for individuals and households.

-1759480422-md.jpg)

-1759480422-sm.jpg)